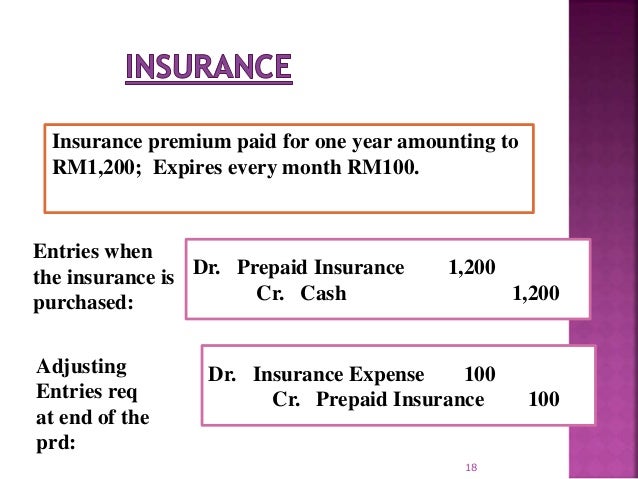

Prepaid Insurance Journal Entry Example : 3 1 A Djustments F Or F Inancial R Eporting Chapter Ppt Download - Prepaid expenses are those which are paid but whose service has not obtained from service provider.

Prepaid Insurance Journal Entry Example : 3 1 A Djustments F Or F Inancial R Eporting Chapter Ppt Download - Prepaid expenses are those which are paid but whose service has not obtained from service provider.. The amount for each is the amount in the example, rs. Insurance premium paid dr the insurance prepaid account and cr the bank account with the actual amount paid to the. This video shows how to record a journal entry for prepaid insurance. ○ if it appears in the trial balance means we had passed journal entry for such stock and adjusted with purchases to calculate cost of. It is a basic skill for bookkeeper to pass journal entry.

Adjusting entries for prepaid expense. Credit mode of payment (cah or bank cheque) rs. Not all insurance payments (premiums) are deductible* business expenses. Prepaid expenses examples accounting for a prepaid expense. The following particulars are ascertained from the book and records.